2015 was a bumper year for Viewpoint‘s EMEA-based collaboration business, with revenues up 48% and a return to operational profitability. According to accounts filed at UK Companies House, total revenue for the year to 31 December 2015 was £11.457m (about US$16.84m or €15.58m at 2015 exchange rates) up from £7.717m in 2014 (post).

2015 was a bumper year for Viewpoint‘s EMEA-based collaboration business, with revenues up 48% and a return to operational profitability. According to accounts filed at UK Companies House, total revenue for the year to 31 December 2015 was £11.457m (about US$16.84m or €15.58m at 2015 exchange rates) up from £7.717m in 2014 (post).

Positive trends

In a conference call last week, Viewpoint’s EMEA commercial director Steve Spark told me that the jump in growth reflected an acceleration in several positive trends including:

- growing adoption of Viewpoint collaboration solution by asset owners (EDF, Emaar and IKEA were mentioned, as were “London-based developers”)

- more consistent approaches to data collection by both Tier 1 main contractors, and Tier 2 contractors (firms with an annual turnover in the range of £100m-£300m); Spark said:

“Willmott Dixon, Carillion, Morgan Sindall and Galliford Try are all enterprise customers using both our Viewpoint for Projects (VfP) and Field View solutions…. Building information modelling, BIM, is acting as a catalyst. We are getting a growing number of approaches specifying compliance with PAS1192, with contractors looking to have a more controlled and consistent approach to document collaboration, common data environments and field data management.”

- growing use of “satellite” collaboration solutions by subcontractors for information management to support civil, structural or MEP work packages.

UK FD Chris Baty said the jump in revenues also marked the first full year of contribution from the former Mobile Computing Systems business (acquired in December 2014) – a third of the 48% could be attributed to Field View revenues, but this still left a very healthy 32% increase in core collaboration revenues for the Newcastle, UK-headquartered business. Company headcount grew from 70 in 2014 to 96 in 2015, with total employee numbers now over the 100 mark despite competitor rumours that the business was losing staff (see 4 May 2016 post).

Underlying trends in system use showed a 26% increase in the number of documents stored on the VfP system, while BIM helped contribute to a 32% increase in the volume of data stored. The number of Field View users was up 26% in a year, with a 45% increase in the number of data capture processes completed.

Spark would not be drawn on detailed performance since the end of the 2015, but said “double digit” growth for 2016 was “very encouraging”, with no impact detected as yet from Brexit-related uncertainty. Internationally, the company was doing “incredibly well” in the Middle East, and had been growing its partner network in mainland Europe.

Exceptional item

In 2014, Viewpoint reported its first loss after seven consecutive years of £1m-plus profits, mainly due to a sharp increase in headcount, plus investments in R&D and in marketing in the US and Australia.

The company returned an operating profit of £0.367m in 2015, but this was wiped out by an £0.742m exceptional item (“relating to legal and other costs incurred in the year to settle a legal dispute”), resulting in reported pre-tax loss of £0.375m. The Viewpoint team said they could not comment on this item due to a confidentiality clause, but I believe this relates to the July 2015 settlement of an action brought by Melbourne-based Project Collaboration (see 4Projects facing Au$9m reseller claim).

Enterprise adoption

US Viewpoint executives were also on the conference call, and CEO Manolis Kotzabasakis highlighted another dimension of Viewpoint’s UK growth: enterprise-level adoption. He told me:

“We have seen significant movement from project-based collaboration to enterprise deals. At one time, UK construction project managers regarded collaboration as good but optional; now they see it as mandatory and standard across all their projects. In the US, we are also seeing growing interest in VfP and Field View from US contractors looking to adopt Viewpoint for ERP.”

Spark reckoned that around 75% of VfP and FV revenues were now flowing from enterprise deals.

The Viewpoint for Projects and Field View operation is, of course, just part of a much bigger US-headquartered business now employing over 700 people worldwide. At the time of a US$230m investment from Bain Capital in April 2014, the business, which provides financial compliance, project management, estimating, and content management software as well as project collaboration, BIM and mobile tools, was forecasting revenues of US$140m. For 2016, global Viewpoint revenues are forecast to be nearly US$150m.

Digital transformation

In the week when the next phase of the UK’s Digital Built Britain programme (post) was announced (news release), Kotzabasakis also highlighted how digital transformation was now beginning to influence IT investments by construction businesses on both sides of the Atlantic. He said the latest Viewpoint user conference had been the most successful yet, with 1700 delegates in attendance and 53 partners exhibiting at the Portland, Oregon event, and his keynote had highlighted the opportunity for construction to raise its game through digitisation (we briefly disussed recent McKinsey reports showing construction lagging behind other industries in terms of its digital transformation; see also Construction mainly technology laggards).

His Viewpoint colleague Maury Plumlee, VP of global marketing, said construction was beginning to move forward with digitisation because the AEC information technology ecosystem is becoming less fragmented. A veteran watcher of the ERP space, he recalled that the US construction ERP space in 2000 had about 20 software providers specialising in AEC ERP, in addition to generic ERP solution providers. This number was now down to six or seven, he said, meaning some vendors now had the necessary critical mass to bring about change across the construction supply chain (a view shared by Kotzabasakis in May 2016). The UK was leading on digital transformation due to its headstart with BIM but the US was also “really heating up” I was told.

Competitive comparisons

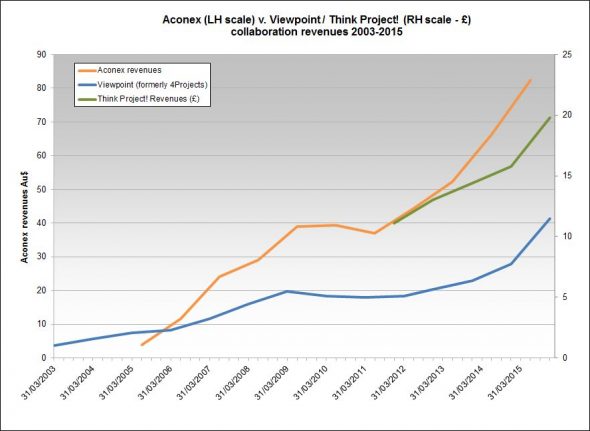

Inevitably, comparisons will be made between the performance of Viewpoint and those of construction SaaS competitors, particularly Australia’s Aconex. In the year to 30 June 2016, Aconex announced underlying organic revenue growth of 31%, with the acquisition of Conject boosting total revenue growth to 50% (read Conject deal boosts Aconex revenue growth). Viewpoint matches these figures closely – underlying growth of 32% with the MCS acquisition pushing total growth to 48%. Earlier this year, Germany’s Think Project! reported 2015 revenue growth of 33% (post), so we have something of a benchmark of 30%-plus revenue growth to use to assess others’ performance. Of course, the scale differs but recent revenue trajectories across the three businesses appear very similar (see below); at the top of the market, this looks currently to be a buoyant and fast-growing sector.

1 ping

[…] « Viewpoint UK revenues up 48% in 2015 […]