SaaS construction collaboration vendor 4Projects grew its revenues 21% in the year ending 31 December 2014, but also reported the business’s first significant loss.

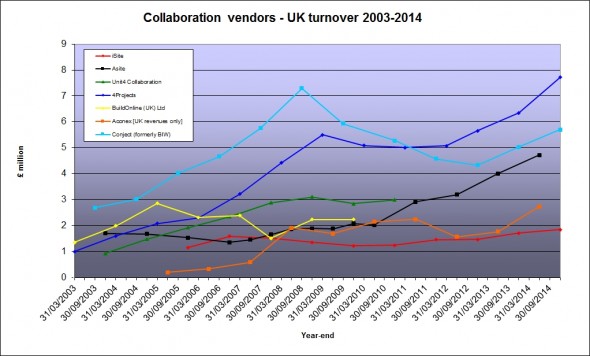

The Newcastle, UK-based SaaS construction collaboration technology vendor 4Projects (now Viewpoint for Projects) grew its revenues 21.5% in the year ending 31 December 2014. The UK subsidiary of Portland, Oregon, US-based Viewpoint Construction Software has filed its annual report and accounts at Companies House, and they show revenues increasing from £6.351m in 2013 to £7.717m (c. US$11.99m or €9.86m) last year, during which, in December 2014, the company acquired Mobile Computing Systems.

The Newcastle, UK-based SaaS construction collaboration technology vendor 4Projects (now Viewpoint for Projects) grew its revenues 21.5% in the year ending 31 December 2014. The UK subsidiary of Portland, Oregon, US-based Viewpoint Construction Software has filed its annual report and accounts at Companies House, and they show revenues increasing from £6.351m in 2013 to £7.717m (c. US$11.99m or €9.86m) last year, during which, in December 2014, the company acquired Mobile Computing Systems.

First loss

However, this acquisition does not account for the company’s first reported loss. After seven consecutive years of £1m-plus profits, the business has reported a pre-tax loss of £1.046m (c. US$1.62m or €1.34m) in 2014, compared to a £1.597m profit in 2013. The accounts show a sharp increase in headcount from 57 to 70, and a corresponding jump in payroll costs of around £0.9m, but these only partially account for the dip. The report explains this as follows:

“[There was] continued and sustained investment in all parts of the business. In particular the group invested significantly in R&D and growing our North American and Australian businesses to leverage our parent company’s significant presence in those markets. Given the subscription nature of our revenue the return on this intercompany investment will be felt more keenly in future years and in 2014 resulted in a planned accounting loss easily covered by our strong balance sheet.

Our investments in 2014 continue at a pace in 2015 and are already paying off in 2015 with strong growth continuing across all of the regions in which we sell.

4Projects saw revenues up around 14% in the UK (accounting for 75% of the company’s business), and up over 50% from the rest of the world, albeit from a relatively low starting point, said finance director Chris Baty. The Middle East was “undoubtedly strong”, and the growth had continued in 2015 (and “has the potential to accelerate again in 2016”). UK revenue growth is already accelerating, UK MD Alun Baker told me: “it’s above 20% and we’re seeing significant growth in infrastructure business”.

Product portfolio

As well as international expansion, the business has also been expanding its product portfolio, Alun said. “4Projects used to sell just a single product; now we have three new areas: our mobile capabilities, our BIM capabilities, and, in the US, integration into Vista ERP.” He said this was “proving increasingly attractive to many contractor customers who are now looking more strategically at their IT portfolio, looking to integrate documents, BIM, site activities and back office.” He also feels Viewpoint for Projects is the “SaaS leader in the BIM marketplace.”

As well as international expansion, the business has also been expanding its product portfolio, Alun said. “4Projects used to sell just a single product; now we have three new areas: our mobile capabilities, our BIM capabilities, and, in the US, integration into Vista ERP.” He said this was “proving increasingly attractive to many contractor customers who are now looking more strategically at their IT portfolio, looking to integrate documents, BIM, site activities and back office.” He also feels Viewpoint for Projects is the “SaaS leader in the BIM marketplace.”

The 4Projects integration of MCS’s former Priority1, now Field View, into the product porfolio is “proving compelling in the market place,” according to the report. Baker says it was an important milestone for 4Projects, and after unifying sales and support functions, rebranding and promoting the combined offer, “it’s proved a very successful acquisition for us, with 50% growth in revenues this year and big international interest”.

Price pressure?

I asked Alun about competitive pressures (highlighted by Conject UK in their recent annual report; post). Not naming names, he told me:

“We find some competitors in their native geographies are defending their positions at the market rate, but when it comes to winning work in other markets it’s different. In the UK, we’ve seen them offer significant – and, in our view, unsustainable – reductions.”

He underlined again the attractiveness of the integrated Viewpoint for Projects portfolio to contractors and other customers. “This is allowing us to sustain our price point, and we have seen an increase in both our average order value and the duration of contracts.”

Mindful of US GAAP reporting rules, he would not be drawn on the size of the business’s order book, but said the company had seen its net actual new contract value totals tracking at over 140% of plan. This was encouraging Viewpoint – buoyed by its investment from Bain Capital – to invest in maintaining the SaaS business’s revenues, as these were distinctly different in character to revenues derived from traditional perpetual licenses.

Commentary

Allowing for the different reporting periods, ViewPoint for Projects’ 21.5% growth in 2014 plus its talk of accelerating growth in 2015, compares well to the 24% growth achieved by its international rival Aconex in the year to 30 June 2015. AEC SaaS vendors are growing revenues modestly in established markets such as the UK and mainland Europe (4Projects’ 14% UK growth is consistent with the 13% achieved by both Conject UK and Germany’s think project!), but – clearly – expanding into the Middle East and other developing markets is the key to significant revenue growth.

However, such expansion can hit profits. Australia-based Aconex’s experience suggests establishing a strong presence in a new market like north America requires significant investment in personnel and infrastructure, and attractive pricing to encourage early adoption. As a result, it may take time for that investment to generate a strong contribution to the bottom line (this Sydney Morning Herald article points out Aconex still lost Au$8m before tax [and accounting adjustments] in a market which remains a volatile ‘landgrab’ and where “being too conservative will almost certainly spell long term failure”).

I also note some convergence in the product strategies of these major players. With file sharing and document collaboration increasingly commoditised and rising competition at the SME end of the market (as well as ‘freemium’ solutions like GenieBelt, I have seen many low-cost solutions launched – a $15/user/month from BlueVue is just one recent example), the leading SaaS vendors are looking at the richer pickings of the enterprise market. They are marketing an expanded portfolio of services: workflow, mobile tools, BIM, integration with back office, business intelligence and financial reporting. With the UK government BIM mandate due to come into force in 2016 (and other countries following suit (eg: France 2017, Spain 2018), such more holistic offerings are likely to become more widely used. And the fruits of 4Projects’ prolonged investment in BIM could help boost its UK revenues, and make it attractive to customers and supply chains looking to deploy BIM in other markets.

London: 3pm GMT – CEO Greg Bentley opened today’s press conference with a brief mention of the US company’s declared intention (July 2015) to float on the stock exchange, but quickly dampened speculation by saying that Wall Street sentiment towards IPOs had chilled in recent months. Instead, therefore, he focused on the company’s acquisitions over the past year – including that of EADOC in March 2015 (see also April 2015 post: Law expands on Bentley’s EADOC deal) – and then a series of recent announcements.

London: 3pm GMT – CEO Greg Bentley opened today’s press conference with a brief mention of the US company’s declared intention (July 2015) to float on the stock exchange, but quickly dampened speculation by saying that Wall Street sentiment towards IPOs had chilled in recent months. Instead, therefore, he focused on the company’s acquisitions over the past year – including that of EADOC in March 2015 (see also April 2015 post: Law expands on Bentley’s EADOC deal) – and then a series of recent announcements. Now, with ProjectWise CONNECT Edition, this “workhorse for work sharing”, “the ‘gold standard’ for AECO collaboration worldwide” (Bentley’s words) is now available to the entire supply chain, taking advantage of Bentley’s Microsoft partnership using the Azure cloud-computing platform. Senior Vice President Bhupinder Singh highlighted the company’s cloud services as core to the triple challenges of increasing complexity of devices, software and data.

Now, with ProjectWise CONNECT Edition, this “workhorse for work sharing”, “the ‘gold standard’ for AECO collaboration worldwide” (Bentley’s words) is now available to the entire supply chain, taking advantage of Bentley’s Microsoft partnership using the Azure cloud-computing platform. Senior Vice President Bhupinder Singh highlighted the company’s cloud services as core to the triple challenges of increasing complexity of devices, software and data. A major benefit of all Newforma solutions is each product is designed to help customers save time completing many of the processes they deal with every day. In doing so, Newforma’s products eliminate waste and allow our customers to add value to their customers. Eliminating waste/ adding value are two tenets of lean, and LeanPlanner was created to specifically address these two processes.

A major benefit of all Newforma solutions is each product is designed to help customers save time completing many of the processes they deal with every day. In doing so, Newforma’s products eliminate waste and allow our customers to add value to their customers. Eliminating waste/ adding value are two tenets of lean, and LeanPlanner was created to specifically address these two processes. A news release just in from

A news release just in from  Woking, Surrey-based SaaS construction collaboration vendor Conject UK, the British subsidiary of the Munich, Germany-based

Woking, Surrey-based SaaS construction collaboration vendor Conject UK, the British subsidiary of the Munich, Germany-based

Operations in Singapore continued to expand, while “the Middle East, was, and remains, very active,” though “some contracts took some considerable time to conclude, resulting in a number of delays to project commencement dates” (and presumably reducing revenues).

Operations in Singapore continued to expand, while “the Middle East, was, and remains, very active,” though “some contracts took some considerable time to conclude, resulting in a number of delays to project commencement dates” (and presumably reducing revenues).