Australia is fertile territory for mobile construction technology businesses. APE Mobile is a Perth, WA-based start-up automating contractors’ paperwork requirements.

![]() It’s a familiar story. Experienced construction professional wants to use a mobile device; tests some examples and finds none of them do what he thinks is necessary; decides to develop his own mobile software instead.

It’s a familiar story. Experienced construction professional wants to use a mobile device; tests some examples and finds none of them do what he thinks is necessary; decides to develop his own mobile software instead.

Matt Edwards, a former Siemens Building Technologies executive with experience in the UK and Europe before moving to Australia, established a construction business consultancy called Applied Project Experience in Melbourne in 2009, and then moved to Perth. Following the launch of the Apple iPad tablet, he then began looking at the use of mobile technology to support construction business processes and developed a prototype application, called APE Mobile.

While his initial effort was, on his own admission, “a bit flaky”, he was encouraged enough to bring in a specialist software developer, David Hayward (founder and developer of ER Mapper, later ERDAS), and in November 2013, the first production release of APE Mobile’s Paperless Site app for contractors was launched. Contractor reaction to the Software-as-a-Service app was immediately positive, and the company quickly signed up several well-known international and Australian client businesses, including RioTinto, Colas and Monadelphous, plus a host of small- and medium-sized contractor businesses (see Tasman Civil case study).

“Not a collaboration tool”

“Not a collaboration tool”

“APE Mobile is not a collaboration tool, at least not like Aconex,” Matt says. “It’s a tool for individual contractors to help them manage their own documents and processes across their project portfolio”. The application is broadly divided into five areas:

- Memos – includes RFIs, site instruction, records of conversations, and captured responses

- Forms – for internal paperwork

- Actions – for defects, Non-Conformance Reports, etc

- Drawings & Docs – includes annotation tools

- Reports – for punchlists, custom reports, exports.

Adopting a single tenancy approach (creating dedicated storage spaces for each customer), APE Mobile hosts the application and collated information in a secure data centre so that the contractors don’t need to worry about data management; instead, their users can focus on using the mobile application to manage typical site information needs, including safety reporting, site diaries, etc, accessing and annotating drawings and other documents as necessary. The web-based back-end of the application can also be accessed by office-based users from laptops or desktops for administration purposes, and has most of the functions of the iPad app (“the office user can fill in and send forms; you can even start them on the iPad, save as draft, and complete them on the web, or vice versa”).

The mobile app is currently only available for Apple iOS device users (Matt says they have yet to lose a sale because the app isn’t available on, say, Android or Windows), and has been designed to work even when there is no internet connectivity. All the information a user needs can be synchronised to the device, and either updated in the background where 3G signals are available, or synchronised once connectivity is regained (“useful when you are working on a remote mining project beyond the range of mobile devices”).

The mobile app is currently only available for Apple iOS device users (Matt says they have yet to lose a sale because the app isn’t available on, say, Android or Windows), and has been designed to work even when there is no internet connectivity. All the information a user needs can be synchronised to the device, and either updated in the background where 3G signals are available, or synchronised once connectivity is regained (“useful when you are working on a remote mining project beyond the range of mobile devices”).

APE Mobile has been designed to be simple and intuitive to use. It includes form-builder tools so that familiar, previously paper-based processes are faithfully replicated online (“users are essentially doing their own paperwork, only more efficiently because of the automated data entry, drop-down menus, pick-lists, etc”), and is extensively configurable to suit different organisations’ needs without customisation of the core code. An open API enables easy data exchange with back-office business systems, ranging from ERP to Excel spreadsheets, while notifications to external users can be sent via email.

APE Mobile has extended beyond its Western Australia heartland and through recommendation and word-of-mouth has secured adoption by firms on the east coast of Australia. Encouraged by this, Matt is looking at funding options to expand the reach of the business, including taking it into new international markets, perhaps through partnerships with resellers or vendors of complementary technologies (and Matt includes SaaS collaboration platforms in this category). A free trial is available, with individual users supported from $65 per month, plus standard monthly storage allowances based on 10, 25 or 50 users (dubbed Gibbon, Chimp and Gorilla); enterprise deals (surely, King Kong!) can also be negotiated.

My view

The appetite for mobile-centric construction applications is clearly international. As I mentioned last week following my brief look at Basestone 2.0, there is a lot of development activity in the mobile arena – from BIM authoring software vendors, established SaaS players, long-time mobile specialists, plus startups. APE Mobile clearly fits into the latter category, alongside startups in the US, UK and mainland Europe, but – unlike most of these – it isn’t trying to compete with the collaboration vendors. Instead, Matt sees APE Mobile as complementing existing solutions, which may be a better recipe for survival.

Choice of device/operating system will also be a factor in the business’s future. The iPad may dominate site use among APE Mobile’s current Australian customers, but it may well be a different picture if/when APE ventures into, say, south-east Asia where Android use in construction is more widespread.

Richard Waterhouse (right), chief executive of RIBA Enterprises, which owns NBS said, “We already have the backing of key organisations such as CIBSE, CIOB, ICE, IStructE, RIBA and RICS and we will be extending and widening this dialogue over the coming months.” The institutions will form part of a toolkit advisory board providing direction and also potentially undertake subcontracted work.

Richard Waterhouse (right), chief executive of RIBA Enterprises, which owns NBS said, “We already have the backing of key organisations such as CIBSE, CIOB, ICE, IStructE, RIBA and RICS and we will be extending and widening this dialogue over the coming months.” The institutions will form part of a toolkit advisory board providing direction and also potentially undertake subcontracted work. After meeting Blue Ronin/

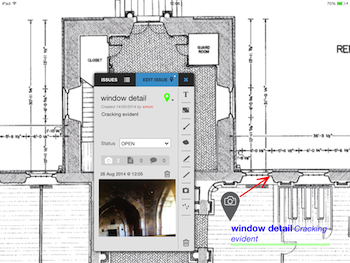

After meeting Blue Ronin/ Information about a single issue is grouped together, aggregating data from multiple Basestone annotation tools and photos, allowing users to capture the progress of an issue from beginning to end, including interim snagging, and ‘before’ and ‘after’ photos. With the issues list, it’s now also easier to get an overview of all issues related to a particular drawing: who created them, how urgent they are and what their status is: simply tap on any issue to zoom into the detail.

Information about a single issue is grouped together, aggregating data from multiple Basestone annotation tools and photos, allowing users to capture the progress of an issue from beginning to end, including interim snagging, and ‘before’ and ‘after’ photos. With the issues list, it’s now also easier to get an overview of all issues related to a particular drawing: who created them, how urgent they are and what their status is: simply tap on any issue to zoom into the detail. Newforma is not about to become a hardware vendor. While SmartUse’s A0 smartboards make it easy to view drawings full-size in the construction site office, the market for the product is already becoming ‘commoditised’ – many existing offices have smartboards already, there are other products in the market, and prices are dropping. The deal was about acquiring mobile-oriented software that could help users view drawings on any smartboard, plus a range of other mobile devices, Ian said.

Newforma is not about to become a hardware vendor. While SmartUse’s A0 smartboards make it easy to view drawings full-size in the construction site office, the market for the product is already becoming ‘commoditised’ – many existing offices have smartboards already, there are other products in the market, and prices are dropping. The deal was about acquiring mobile-oriented software that could help users view drawings on any smartboard, plus a range of other mobile devices, Ian said.

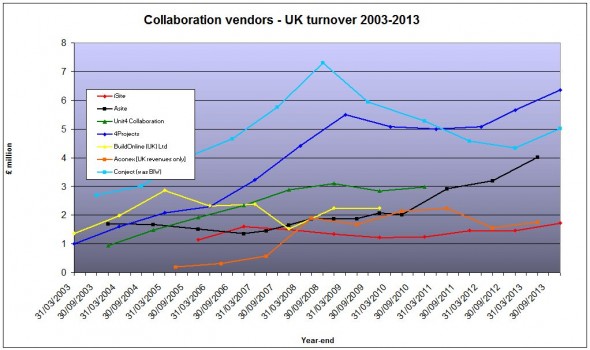

Newcastle, UK-based SaaS construction collaboration technology develop

Newcastle, UK-based SaaS construction collaboration technology develop

4BIM

4BIM “Our customers and the construction market recognize the commitment we are making to both product and team development and this shows in the number of new customers we’ve gained over the year. Much of our growth has been seen in greater adoption by asset owners and operators using the product in both the pre- and post- construction phases of the asset lifecycle, and also customers adopting the product at an enterprise level versus on a project basis. We have also recently increased investments in expanding and developing both our direct sales channel and our international channel partner programme.”

“Our customers and the construction market recognize the commitment we are making to both product and team development and this shows in the number of new customers we’ve gained over the year. Much of our growth has been seen in greater adoption by asset owners and operators using the product in both the pre- and post- construction phases of the asset lifecycle, and also customers adopting the product at an enterprise level versus on a project basis. We have also recently increased investments in expanding and developing both our direct sales channel and our international channel partner programme.” Accelerating adoption of SaaS – While there is a large installed base of conventional client/server software, SaaS solutions (and similar subscription-based approaches) spread software costs over a longer period and reduce internal IT management overheads. Existing trends away from internal electronic document management systems (EDMSs) towards externally hosted platforms will continue. Similarly, use of document-centric collaboration will, over time, shift towards owner-operator adoption of model- and data-centric SaaS ILM platforms (first CDEs, and later Level 3 or iBIM) – but there won’t be a sudden UK “BIM boom” for the SaaS vendors in 2016. More likely, there will be a gradual ramp up as centrally-procured public sector (and some early adopter private sector clients) projects start to require CDEs.

Accelerating adoption of SaaS – While there is a large installed base of conventional client/server software, SaaS solutions (and similar subscription-based approaches) spread software costs over a longer period and reduce internal IT management overheads. Existing trends away from internal electronic document management systems (EDMSs) towards externally hosted platforms will continue. Similarly, use of document-centric collaboration will, over time, shift towards owner-operator adoption of model- and data-centric SaaS ILM platforms (first CDEs, and later Level 3 or iBIM) – but there won’t be a sudden UK “BIM boom” for the SaaS vendors in 2016. More likely, there will be a gradual ramp up as centrally-procured public sector (and some early adopter private sector clients) projects start to require CDEs. “The SmartUse app is the most advanced mobile solution for viewing, marking up, auto-linking and sharing project plans. It allows contractors and owners to easily review plans on computers in their offices or on tablets on the job site. Because it also operates on a large, 55-inch touch screen, SmartUse enables an entire project team to interact with a set of documents as they collaborate in real time in a project office or job trailer. We are excited to add this new product to help contractors and owners better manage the thousands of plans they keep and reference for all of their projects. We are also delighted to welcome the extremely talented employees of SmartUse to the Newforma team.”

“The SmartUse app is the most advanced mobile solution for viewing, marking up, auto-linking and sharing project plans. It allows contractors and owners to easily review plans on computers in their offices or on tablets on the job site. Because it also operates on a large, 55-inch touch screen, SmartUse enables an entire project team to interact with a set of documents as they collaborate in real time in a project office or job trailer. We are excited to add this new product to help contractors and owners better manage the thousands of plans they keep and reference for all of their projects. We are also delighted to welcome the extremely talented employees of SmartUse to the Newforma team.”